From Queues to QR Codes: Pakistan's Payment Transformation

Electronic Money Institution - EMI Explained

Hey there 👋

If you ask some of the boomer generation around you, you’d be surprised to know that you had to stand in queues to get your WAPDA bill paid in Pakistan.

You paid in cash. You stood in lines either in banks or offices. You paid money through a guy on the physical counter with a not-so-good mood.

If you wanted a bank account you were in for a treat, because the manager wouldn’t easily open your account unless you were someone with deep pockets (this has somewhat improved though).

And If you were a freelancer earning online, there were simply no options for you until just a few years ago.

Fast forward to today, and millions of Pakistanis send money with a thumbprint. Utility stores now display their Raast QR codes.

Freelancers receive international payments into app-based wallets. And the government openly talks about reducing the country’s dependence on cash (so they could tax us more :p).

We Gen-Z folks certainly have it easy when a lot of what was in-person, painful is now being digitized especially in the financial sector.

At the center of this transformation are digital wallets and Electronic Money Institutions, or EMIs that have led this change for the average consumer.

But to understand what is happening, we first need to understand what an EMI actually is.

Even though I want this piece to be a positive outlook one, rest assured, millions of people still stand in lines and are frustrated by the current landscape as well. Just that it is improving, though at a very slow pace.

So What Is an EMI?

An EMI is a company licensed by the State Bank of Pakistan to issue electronic money. That means it can create a digital wallet for you, store your money digitally, and allow you to send, receive, or spend it through apps, cards, or QR payments.

An Electronic Money Institution is not a bank. It is not a savings account. It is not a loan provider.

The key difference is this: your EMI wallet is designed for movement of money, not multiplication of money. It is built for transactions, not for lending. This is where most people get confused.

From the outside, a wallet app feels like a bank. You have a balance. You can transfer money (to wallets and to banks). EMIs also give out a debit card.

But under the hood, EMIs are restricted from lending money or creating credit the way banks do. They operate under a lighter regulatory framework focused specifically on quick payments.

According to the State Bank of Pakistan’s official list, companies such as SadaPay and NayaPay have EMI licenses, while others remain in pilot or approval stages.

This licensing structure is pretty sensitive. It provides limited control to the EMIs. Although for the average Bashir, this distinction doesn’t matter much.

If you want to pay bills, send or receive funds or use a debit card on Daraz, EMIs would generally work the same way a bank would.

However, EMIs usually have some limits on spending and receiving funds above a certain threshold. It’s usually 300K-500K PKR depending upon the service you’re using.

What EMIs Can Do

From our Bashir’s perspective, the main thing about EMIs is simplicity.

He just has to download an app. Upload his CNIC and selfie and within minutes, he has a working digital wallet.

You can transfer money to friends instantly. You can pay utility bills. You can recharge your mobile balance. You can scan a QR code at a store.

Some wallets like SadaPay and NayaPay issue Visa/Mastercard debit cards that work internationally too.

Integration with Raast changed the game further.

Developed by the SBP, Raast enables real-time transfers between banks and wallets. That means your wallet is no longer isolated. It becomes part of a broader digital payment ecosystem.

And the best thing is that there are no fees for using Raast unlike IBFT. Most of the digital wallets now operate on Raast.

Here is something to note:

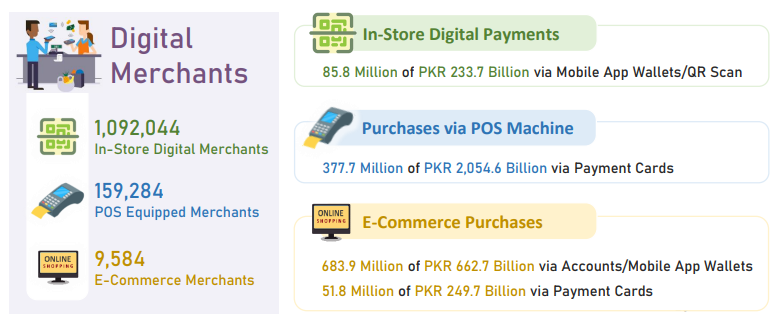

Digital retail payments in Pakistan have surged in recent years, with SBP data showing digital wallets dominating retail transaction volumes.

For the average Bashir, this means less waiting, fewer forms, and fewer physical visits.

For small merchants, it means accepting digital payments without expensive POS machines and catering to those who don’t have cash on hand (like your writer here).

International transactions are really accessible through EMIs. Buying games on Steam is such a breeze on these cards because you can easily freeze them and set spending limits too.

EMIs sold ease of use and people responded. That is their core strength that they’re simple and easy to use for our average Bashir.

What EMIs Cannot Do

Now there are many limits on an EMI when compared to a traditional bank like HBL, UBL, etc.

EMIs cannot lend your deposited money. They cannot offer traditional savings products with interest in the same way banks do.

Basically, they cannot provide large loans from your wallet balance.

This matters because banks generate revenue from lending. They use deposits to create credit. EMIs cannot do lending and that’s why they focus on transaction services.

For the average user, this means if you want a home loan, a car loan, or structured savings products, you still need a bank. Wallets complement banks. They do not replace them.

Understanding this thing is important because it explains Banks and EMIs exist because they have different purposes and limitations.

Why Pakistan Was Ready for EMIs

Pakistan did not become a digital wallet country by accident. The regulation work was already there thanks to the State Bank working hard in the lock-down days.

First, banking penetration was historically low and it was thanks to a number of issues like FATF regulations too. A large portion of the population either did not have bank accounts or did not actively use them.

In 2015, roughly 16% of the adult population had access to bank accounts.

That created a gap. Fintech did not need to replace banks, they just needed to give the users a simpler option.

This number has jumped to 64% by 2025.

Another reason was that Cash has been the king, Pakistan has always been cash heavy because most people just avoid banks whenever they can. You just don’t want to meet a bank guy on a summer afternoon.

When most payments happen in cash, even a small shift toward digital creates explosive growth.

Smartphones also increased this growth because over the past decade, phones have gotten more affordable and expanding 4G coverage made app-based services accessible to millions.

This was the time people started getting familiar with online shopping on Daraz and getting food through Foodpanda.

Add to that Pakistan’s freelancing boom. Pakistan consistently ranks among top freelance markets globally.

But freelancers need digital ecosystems. They need accounts that can receive payments, connect to cards, and function internationally.

Traditional banks were (and still are) often slow or paperwork heavy. Digital wallets just feel a lot smoother than banking apps.

Finally, there is the demographics. Pakistan is young and a large portion of the population grew up with mobile apps, ride hailing, and food delivery. Managing money through a phone just felt natural.

When you combine low banking access, high mobile adoption, freelancing growth, and a young population, EMIs would have naturally found Pakistan either way.

Banks vs EMIs – The Real Difference

From a user experience perspective, banks and EMIs feel miles apart.

Banks require paperwork, stress branch visits, minimum balances, and painfully longer onboarding processes. Just try to get an account opened for the first time as a student.

They are structured institutions designed for full financial intermediation. And sadly, our banks are not incentivized to modernize or focus on retail users because much of their revenue comes from institutional lending.

Our banks lend to our government (yup, it’s crazy, we may cover it someday)

EMI apps are simple, clean and user friendly when compared to traditional banks.

They don’t have minimum balance requirements and they have digital onboarding and no branch visits.

While our banks made billions when the economy crashed EMIs were pushing small updates for our Bashir because he’s their target user.

This is why many people like me treat wallets as daily transaction tools while keeping banks for long-term savings or loans.

It’s not that one is there to replace the other. Both exist with different purposes for me and many others like me.

The Big Digital Wallets in Pakistan

The Early Movers

Easypaisa was among the pioneers of digital wallets platforms in Pakistan.

Launched as a Microfinance Bank, it built massive agent networks especially across urban and rural areas.

To this day, Easypaisa enjoys the First-mover advantage because it is a popular option especially for people who are from rural areas and looking to send funds back to their families.

Today, Easypaisa is not just a digital wallet anymore but it recently became Pakistan’s first digital bank. What this means is that it has the biggest portfolio of services out of the other popular digital wallets.

JazzCash followed Easypaisa as a microfinance bank and it quickly gained a big user-base too because it already was the biggest telecom provider in Pakistan.

Although your writer has had enough bad experiences with JazzCash in the form of occasional payment delays, it is still a giant with millions of registered users.

The Newer EMIs

Then around COVID days came newer EMI players like SadaPay and NayaPay thanks to EMI regulation work done by the then State Bank governor.

These companies positioned themselves as app-first, card-enabled digital wallets focused heavily on freelancers and urban users.

Instead of agent networks, they leaned into digital onboarding, clean UI and their better designed cards.

The competition between these platforms is not just about users anymore. It is about reliability and customer support.

The Profit magazines showed that digital wallet platforms collectively process trillions of rupees annually, making them essential parts of the digital economy.

Why EMIs Became Popular So Fast

The simple answer from a user perspective is that they were simple and easy for the end-user. Here are some of the core drivers of EMIs growth:

Instant onboarding that’s totally digital

No minimum balance requirements

Simple app interfaces

For freelancers, wallet-linked debit cards allowed international transactions and online purchases without navigating traditional banking complexity.

Services like SadaBiz, although short-lived, tried to provide a solution to the freelancer market’s concerns.

SadaPay also tried creating digital spaces for freelancers and money-minded folks on online platforms like Discord but they were eventually left without a vision.

In a country where bank managers just don’t want to open your accounts and the tough regulations too, users simply are content with a simple NayaPay account for their everyday needs.

How Do EMIs Make Money?

Since EMIs cannot lend deposits, their revenue model revolves around transactions.

Every time you swipe a card or pay through a wallet at a merchant, a small interchange fee is generated. Part of that fee goes to the wallet provider.

Merchants may also pay service fees for accepting digital payments. Partnerships with card networks generate revenue sharing.

Scale is everything. High transaction volumes make thin margins sustainable.

Profit has reported that profitability remains a challenge for many EMI players. Some have shut down or struggled to scale. The business model requires constant growth to justify operational costs.

For users, this means free or low-cost services today are supported by backend economics that depend heavily on the number of users.

Are EMIs Safe?

This is a common question and the simple answer again is: Yes.

EMIs are licensed and regulated by the State Bank of Pakistan. They must comply with SBP’s requirements, meaning customer funds are held in regulated structures.

However, EMI wallets are not the same as bank deposits covered under traditional deposit insurance like banks.

The News has reported on SBP revising EMI regulations to strengthen compliance and oversight.

For users, the practical takeaway is this: make sure the EMI you’re using is properly regulated by the State Bank.

Are EMIs Replacing Banks?

Nope, EMIs are not a replacement for banks.

Banks are for lending, savings, and structured financial products like cars, mortgages and so on, while EMIs dominate ease, speed, and mobile-first payments.

Collaboration is visible. Banks partner with fintech companies. Digital banking arms emerge. Payment systems like Raast bridge gaps between institutions.

But you’re not to get your car financed by an EMI anytime soon.

The Bigger Impact on Pakistan

The rise of digital wallets is not just a fintech story. It is an economic transformation story. It shows that if people are provided better service, they’ll jump to it.

Financial inclusion improves when onboarding becomes easier. Small merchants enter the formal digital economy. Freelancers also get the care they deserve.

The government gains transaction visibility and improved documentation.

Dawn and Express Tribune reporting consistently highlight the government’s push toward digitization as a strategy to reduce informality and increase transparency.

The government wants you and me to use EMIs more, just so they have increased visibility on the money flowing in the economy.

What Comes Next?

The future likely includes deeper integration between banks and fintech companies because SBP has started giving out Digital Banking licenses.

We recently saw Easypaisa become a digital bank from just a wallet while international options like Mashreq also just appeared.

In the coming years, the digital banking space seems to be open for competition and innovation especially in the User Experience side, where traditional banks still suck.

Just as international digital banks come in and set the standard, the locals will have to improve on their service, customer support and UI/UX or have their share eaten by the new competitors.

JazzCash and Easypaisa have started offering lending services in the form of micro-loads. That space may also see a lot of growth and we might start to see companies introducing similar services.

Because of a large number of freelancers we may also see more services tailored around receiving money because that is still one of the complaints shared by the community.

Recently, some banks like Meezan and Alfalah have automated the assignment of PRC codes for receiving foreign money.

Such services along with better integrations with foreign wallets like Wise, ElevatePay are improving too.

We already have apps like Daraz or ticketing apps that integrate Easypaisa and similar wallets into their payment form.

My Recent EMI Experience

I am someone who’s been using EMI wallets ever since the first ones like SadaPay and NayaPay came out.

I remember I was among the first ones to receive the black Founders Club debit card by SadaPay and a shirt lol.

I vividly remember how the SadaPay team had an advertised response time of 13 or so seconds and they delivered on that for the first couple of months.

But I feel things have changed, and for the worse especially for SadaPay especially after their acquisition. I’ve personally felt multiple transfer delays and sometimes cancellations too.

And I’m not alone in this, some of my friends report the same experience.

By the way, Just after Papara acquired SadaPay, we talked about the acquisition in Ep 18 of our Tech Made Fun podcast linked here.

However, NayaPay in my recent experience has been more reliable though. The irony is that things were opposite back when SadaPay launched.

Enough of the rant now, let’s talk about some good.

Actually, Digital finance is not that gloomy in Pakistan it seems. We have a really young population with a large number of smartphone users.

That’s why Pakistan’s digital finance market is just too big to ignore. That’s partly why we’re seeing international giants like Mashreq and Papara here.

Even in local space, the very digital wallets that disrupted the scene are now evolving. EasyPaisa which started as a digital wallet, is now a digital bank.

EasyPaisa was the first one and it’s possible we might see NayaPay or others go this route and offer a wider range of services than they currently provide.

And services like Mashreq are already setting the standard for what the average citizen is going to demand from EMIs and banks too.

A friend of mine recently opened an account with Mashreq and was surprised when the on boarding literally took a few minutes. He was able to perform biometrics, verify his picture with NADRA through the app.

He was even able to do Zakat verification completely digitally, which AFAIK no other traditional bank offers at the moment.

And players like Mashreq aren’t an EMI, they are proper banks with saving accounts and other options coming soon which can spell trouble for legacy banks here in the space.

I feel this would give rise to a healthy competition where banks would have to compete with the digital ones in terms of the UI/UX and the one with the best experience and would win users in the long term.

If this trend goes on, not only are we going to have more competitors but also better service from existing ones.

As we’ve repeated in many of our previous articles, competition is good for the end-users. Just take the example of Chinese players entering our automobile market.

As the digital banking license matures it looks like new competitors are going to raise the bar, existing EMI players would adapt and some of them may just become digital banks.

All the while, traditional banks would either have to change themselves significantly or lose the retail market who just isn’t going to accept a 20th century digital experience.

I am hopeful because I’ve gone through the painful process of arguing with branch staff and visiting bank branch multiple times just to get my first bank account opened (looking at you Standard Chartered).

And now seeing that most of this is being replaced with totally digital account opening experiences in minutes makes me happy that even though it took us long at least we’ve got here.